- If You Don’t Control Your Money, It May Control You: 8 Tips For Money Management In a Volatile Market - August 23, 2024

- Breaking Barriers: Women and the Path to Investment Confidence - August 16, 2024

- Turning Fortune into Financial Freedom: A Beneficiary’s Guide to Handling an Inheritance - August 9, 2024

Let’s get something out of the way: Here at Generation Wealth, when we talk about debt, we’re actually talking about interest rates. That’s it. We’re not talking about poor decisions or making you feel bad about trying to get by. That’s what other “money gurus” out there do, and we’re not here for it.

A Different Approach to Debt (That Doesn’t Make You Feel Dumb)

If you’re here, it’s because you’re looking for other alternatives to the traditional debt repayment “wisdom” out there. One common debt repayment tool is called “the baby steps,” which go a little like this:

- Step 1: Save $1,000 ASAP

- Step 2: Pay off all debt, starting with the lowest interest first.

- Step 3: Save 3 to 6 months for your full emergency fund.

- Step 4: Invest 15% of your household income for retirement.

- Step 5: Save for a college fund (because everyone has to have kids apparently).

- Step 6: Pay off your home early.

- Step 7: Build wealth and give (mostly to the church, if you follow their steps exactly).

Do we agree with these steps? Sure… in some ways. But why are these goals tackled one by one? We think you can work on them simultaneously, and with much more success than if you just focus on one of these things at a time.

Instead, we want to take a new approach, one that focuses on interest rates, savings goals, and your lifestyle. So let’s dig into what that looks like and how to get there. Then, we’ll talk about our Three G’s debt plan.

Reframe What Debt Is (NBD)

While we know that some of the “money gurus” out there make millions by saying “Debt is dumb,” we really want you to know: That’s not true. Debt can help you reach certain goals, keep a roof over your head and food on the table… sometimes, debt is necessary. And to be honest, some debt is actually really smart. Hello, mortgages! Generally, we think that high-priority debt (meaning the debt you should pay off faster than the terms/minimum balance) has an interest rate of 6% or higher. This is usually credit cards and some personal loans.

Want to learn more about interest rates and the type of debt you want to pay down first? We have a whole blog about Good, Bad, and Ugly Debt.

Now, Let’s Talk About the Three G’s

So if you don’t need to follow the baby steps in that exact order and if not all debt is dumb…. how should you work on repaying your debt? Is there a way that doesn’t require you to go all-in on your payments at the risk of your comfort or freedom? Yup. We want to talk to you about our proprietary debt plan: The Three G’s.

GATHER — THE COLLECTION PHASE

As we mentioned above, the key to a smart debt payment plan is pinpointing your first debt priorities. Do you have a store credit card that’s charging you 30% interest? Yeah, that has to go. Do you have a car loan at 2.75%? That’s not a priority right now — focus on the minimums and channel the rest of your spare cash to that 30% credit card. Remember, anything above 6% should take priority.

Take a moment to really look at all your debt (we don’t count mortgages in this). List out your credit cards, your student loans, your car loans, your credit lines… whatever extra debt you have. List them out on a piece of paper and include the APR interest rate and the amount owed. Once you have everything listed, look at interest rates first. Move the highest interest rate and balance to the top, and in the next step, we’ll look at how much money you have to channel toward that balance this month (and every month until it’s gone).

GOALS — THE PLANNING PHASE

Now that you know which loans, credit cards, and other debt has a 6% or higher interest rate, let’s look at how you can actually plan to pay it down while funneling money to your savings accounts and other financial goals.

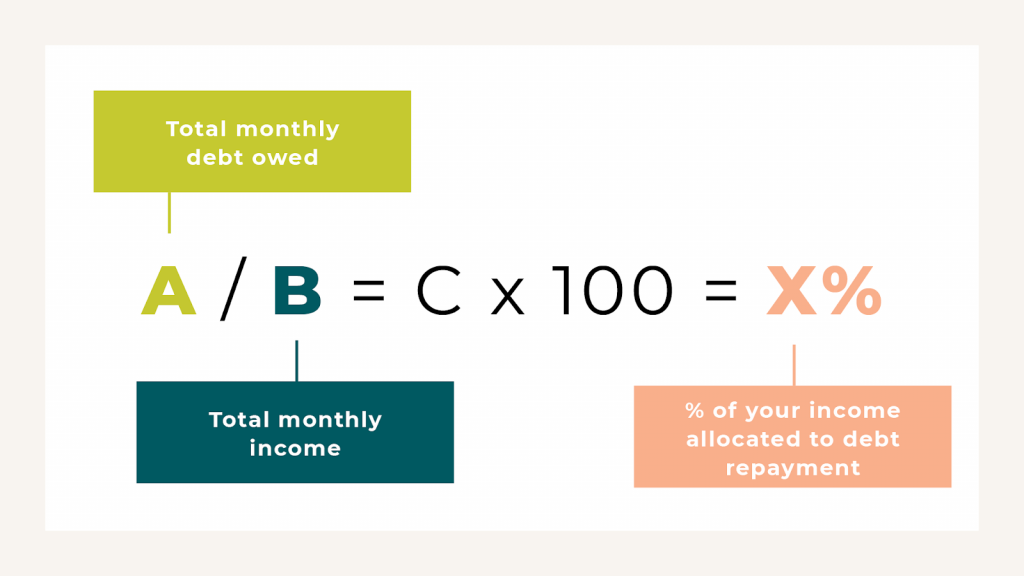

To do this, you’ll want to calculate the percent of your income your debt repayment requires. Here’s a quick calculation to help:

This is the percentage of your income you’ll want to allocate to debt each month. This can also be incredibly helpful if you’re a contract worker or your monthly income varies. If, for example, you find that 10% of your income needs to go to debt repayment, you can allocate 10% of whatever you make each month to debt, even if that final total differs. Just make sure you’re paying the minimums on your low-interest debt, too!

GROWTH — THE ACTION PHASE

Last but not least, this is where you’ll finally start ramping up your debt repayment — without sacrificing your savings! In general, we recommend that 25% of your income goes to saving (and giving!), but if you have a heavy debt load, this may differ. Take a look at how much you’re saving per month (locate the percentage!), and add that to how much you plan to allocate to debt. We know that 40% of your income going to debt and savings may seem like a lot — and it may not be feasible for you. So look at what is realistic, and start creating auto-payments and withdrawals that help you keep those goals.

A mind-blowing thought to leave you with: Debt isn’t your risk. It’s the bank’s.

People think all debt is bad because it’s a financial “burden” that rests on them. But that’s not the truth. The party carrying the real burden are the banks that loan us the money. Essentially, you could never pay that money back (sure, you’d be screwed, but they’d be out the money), so they are the ones more at risk than you are.

Because when we take out loans, we have more money in our bank account. We have more opportunity to do the things that we want to do with our cash. Of course you have to pay everything back within the terms, but that is your leverage.

Debt makes it possible for us to do other things in life, like buy a house, have a baby, build a business, etc. We’re not saying don’t pay down your debt, or to only ever pay the minimums. What we are saying is to use debt wisely, and to not put yourself at risk trying to pay it off — when the risk isn’t yours in the first place!

Want to get crystal clear on your emergency fund numbers, savings goals and a debt repayment plan that works for you? Then join the Know Your Numbers email series.